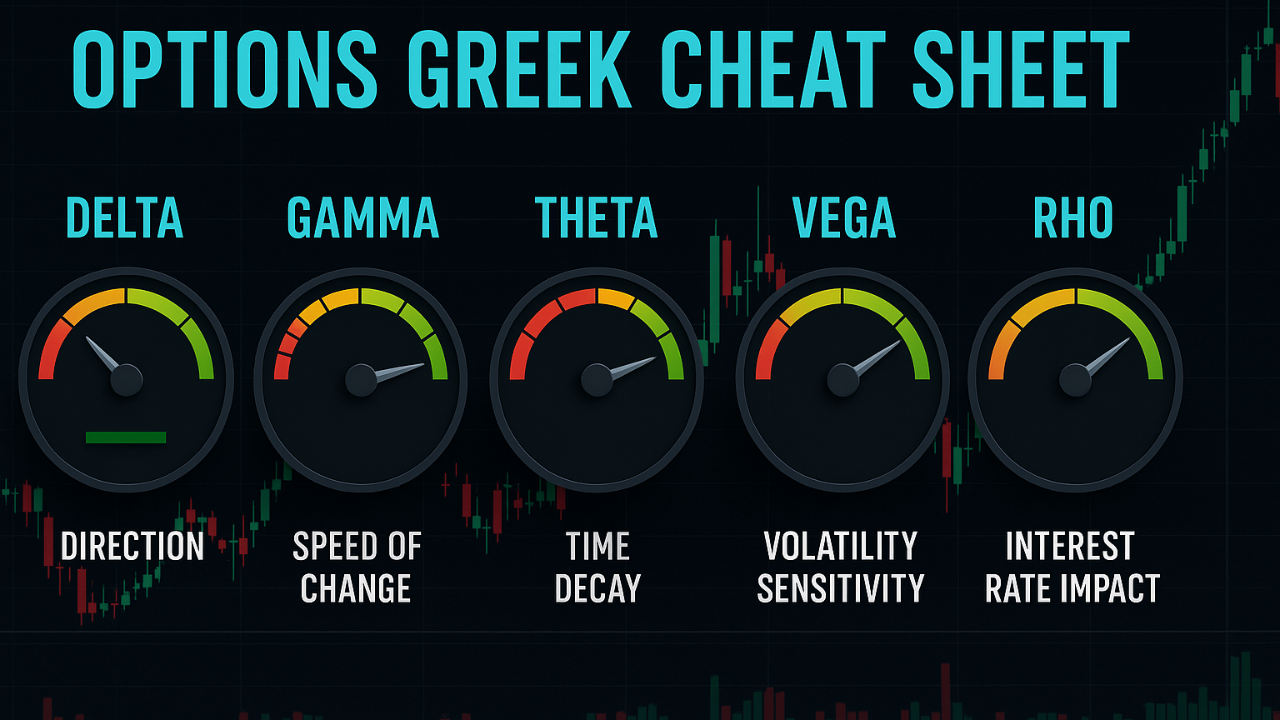

Options Greek Cheat Sheet

This cheat sheet is the complete reference for the five standard options Greeks: Delta, Gamma, Theta, Vega, and Rho. Each section gives you the definition, the characteristics that matter in a real position, a worked example with the actual numbers, and a chart, so you can see how these metrics move option prices and shape your strategy.

Key Takeaways

✅ Delta measures how much an option moves per $1 change in the stock, and doubles as a rough probability of profit.

✅ Gamma shows how fast Delta itself changes; it is highest for at-the-money options and adds volatility risk.

✅ Theta is daily time decay. It accelerates as expiration nears, hurting buyers and helping sellers.

✅ Vega measures sensitivity to implied volatility, which can move option prices even when the stock does not move.

✅ Rho (interest-rate sensitivity) matters least for short-term traders but rounds out the five standard Greeks.

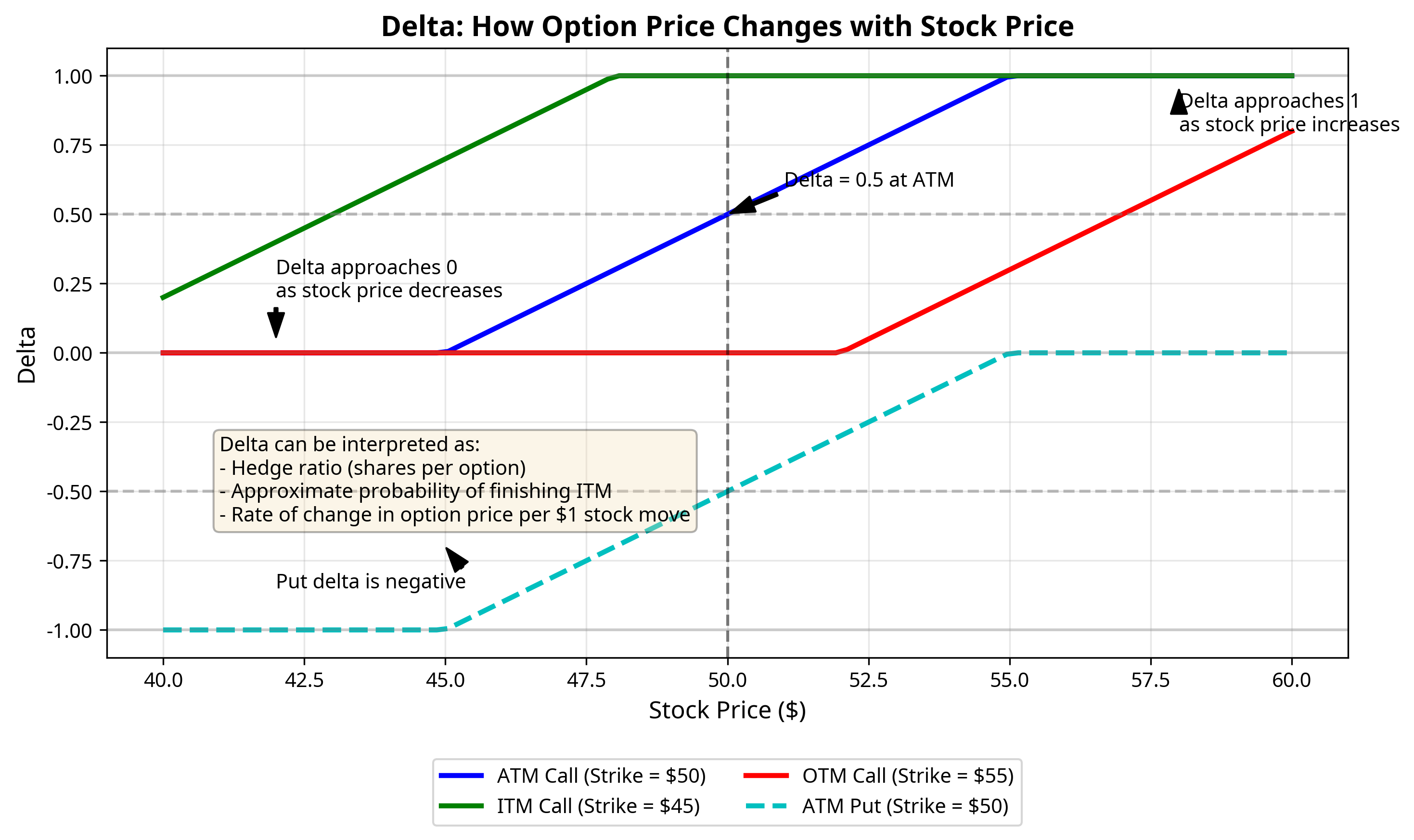

Delta (Δ)

>Δ Definition

Delta is often said to be the most important of the Greeks. It measures the change in an option's price from a change in the underlying security.

Characteristics

- For call options, delta ranges from 0 to +1.00

- For put options, delta ranges from 0 to -1.00

- A delta of 0.50 means the option price will move about 50 cents for every $1 change in the stock price

Practical Example

If you own a call option with a delta of 0.40 and the stock price increases by $1, your option should gain about 40 cents in value (provided the other Greeks remain the same).

The opposite happens if the stock falls—you'd lose about 40 cents.

Delta as an Indicator of Probability

Many traders also use delta as a rough gauge of the probability that an option will be profitable at expiration:

- A call option with a 0.30 delta suggests about a 30% chance of being profitable at expiration.

- A call option with a 0.70 delta suggests about a 70% chance of being profitable at expiration.

- At-the-money options typically have deltas around 0.50, suggesting a 50/50 chance.

This generally means traders can use delta to measure the directional risk of a given option or options strategy.

Higher deltas may be suitable for higher-risk, higher-reward strategies that are more speculative, while lower deltas may be ideally suited for lower-risk strategies with high win rates.

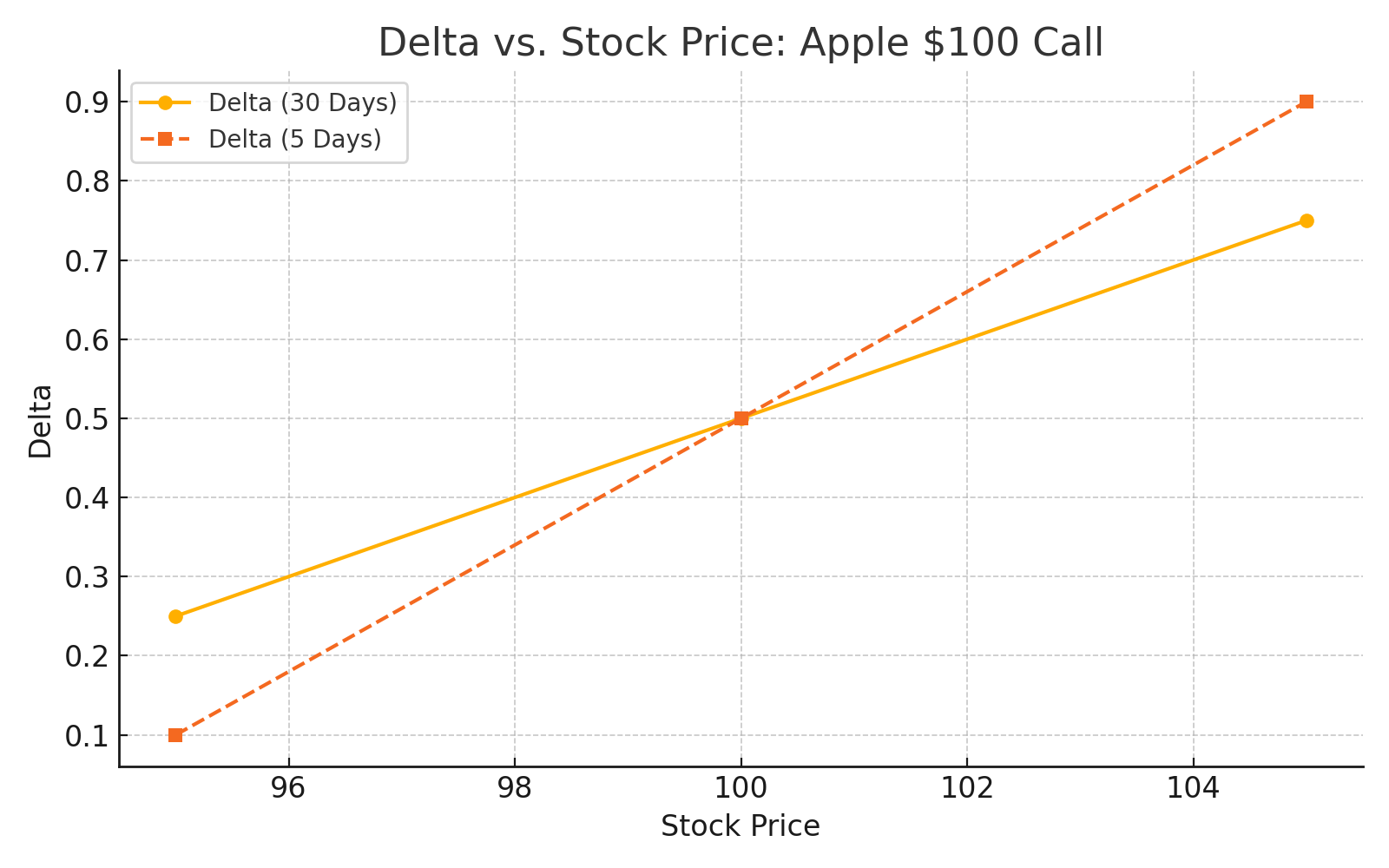

Delta in Action: Apple $100 Call Example

Let's analyze a $100 call on Apple (AAPL) at various stock prices and expiration dates. This shows how Delta shifts as the option moves in or out of the money, and as expiration approaches.

Chart: Delta vs. Stock Price

How Traders Use Delta

⚡ A deep in-the-money call (Delta 0.80+) moves almost dollar-for-dollar with the stock, which suits a strong directional view.

⚡ A 0.20 Delta put you sell carries roughly an 80% probability of expiring worthless, and a 20% chance it does not.

⚡ Delta is also a position-sizing tool: five contracts at 0.20 Delta give you about the same exposure as 100 shares.

Gamma (Γ)

Γ Definition

Gamma tells you how quickly delta will change when the stock price moves. Gamma values are highest for at-the-money options and lowest for those deep in-the-money (ITM) or out-of-the-money (OTM).

Characteristics

- Gamma is always positive for long options (whether calls or puts)

- Gamma is always negative for short options

- Gamma is highest for at-the-money options

- Gamma approaches zero for deep ITM or OTM options

Practical Example

Let's say you own a call option with the following details:

- Delta: 0.50

- Gamma: 0.05

If the stock rises $1, then the following occurs:

- Delta will increase by about 0.05 to 0.55

- Your option will gain about 50 cents from the initial move

- Future moves will have a slightly bigger impact because of the higher delta

Risk Implications

Suppose that two options have the same delta value, but one option has a high gamma, and one has a low gamma. The option with the higher gamma will have a higher risk since an unfavorable move in the underlying asset will have an oversized impact.

High gamma values mean that the option tends to experience volatile swings, which is bad for traders looking for predictable prospects.

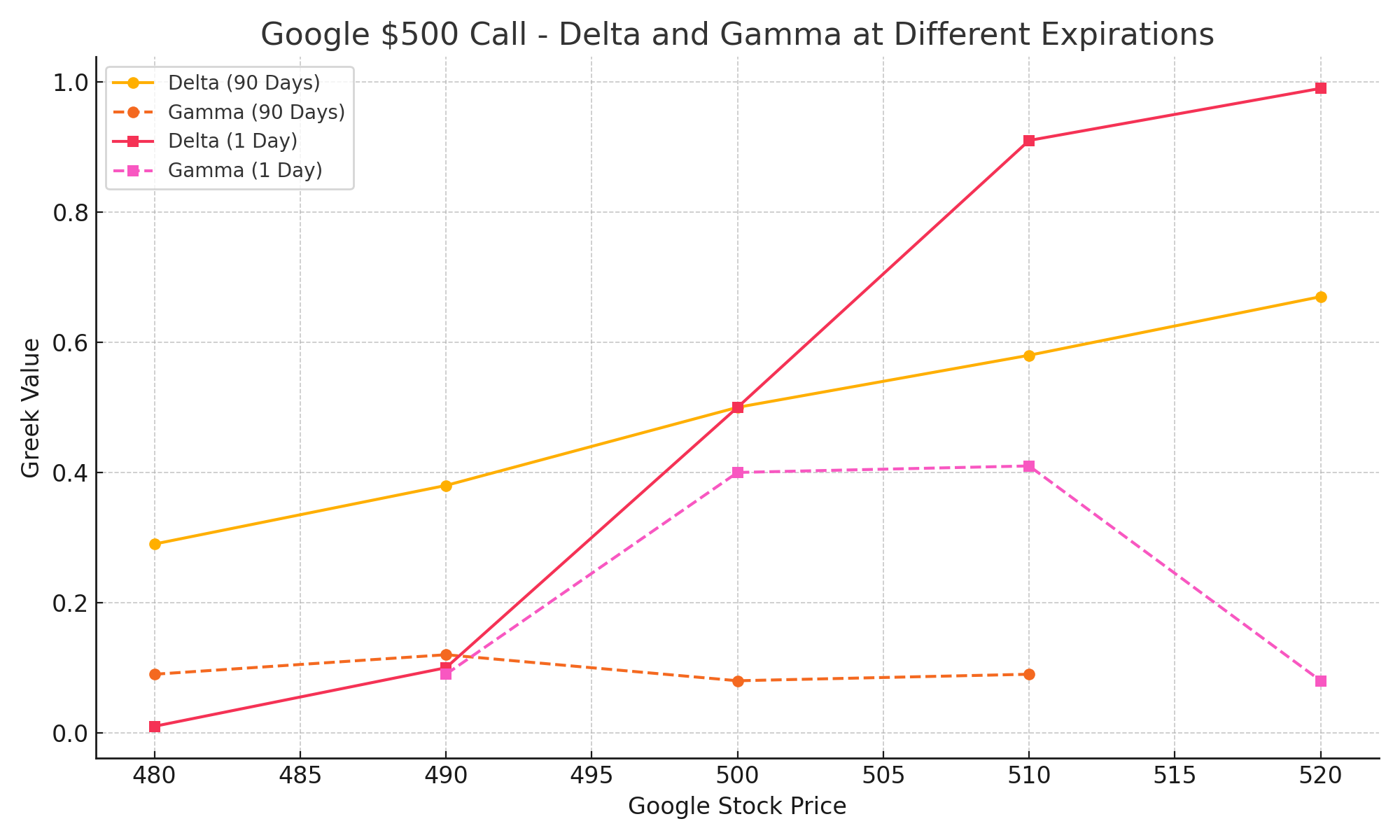

Gamma in Action: Google $500 Calls at 90 Days vs. 1 Day

Let's compare how Gamma behaves for a $500 Google call option with 90 days until expiration versus 1 day until expiration.

90 Days Until Expiration

1 Day Until Expiration

Chart: Delta and Gamma at Different Expirations

How Traders Use Gamma

⚡ Shorter-dated options carry higher Gamma, especially at the money, so Delta moves faster as the stock moves.

⚡ If you are buying options, high Gamma works for you: get the direction right and the position accelerates.

⚡ If you are selling options, high Gamma is the risk. Delta grows quickly against you, which is why short positions get twitchy near expiration.

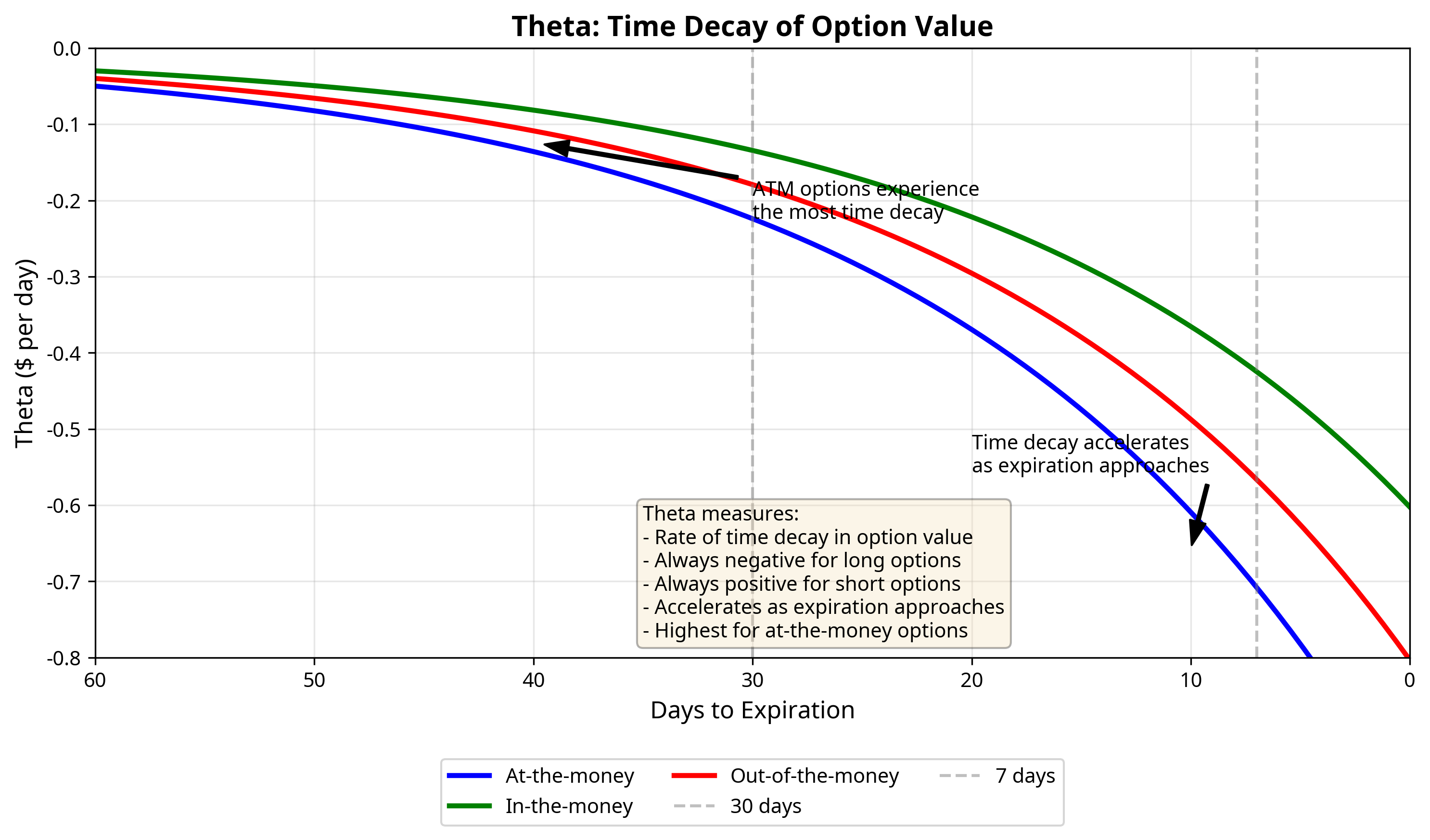

Theta (Θ)

Θ Definition

Theta measures the rate of time decay in the value of an option or its premium. It quantifies how much an option's price will decrease as time passes.

Characteristics

- As time passes, the chance of an option being profitable or in-the-money decreases

- Time decay tends to accelerate as the expiration date draws closer

- Theta is always negative since time moves in the same direction

- Theta is generally good for sellers and bad for buyers

Practical Example

An option premium with no intrinsic value will decline at an increasing rate as expiration nears.

The table below shows theta values at different time intervals for an S&P 500 Dec at-the-money call option with a strike price of 930:

As you can see, theta increases as the expiration date gets closer. At T+19 (six days before expiration), theta has reached 93.3, which means the option is now losing $93.30 per day, up from $45.40 per day at T+0 when the hypothetical trader opened the position.

Trading Implications

Option buyers face a constant battle against time decay, while option sellers benefit from the passage of time. At-the-money options typically experience the most significant time decay, and this decay accelerates in the final weeks before expiration.

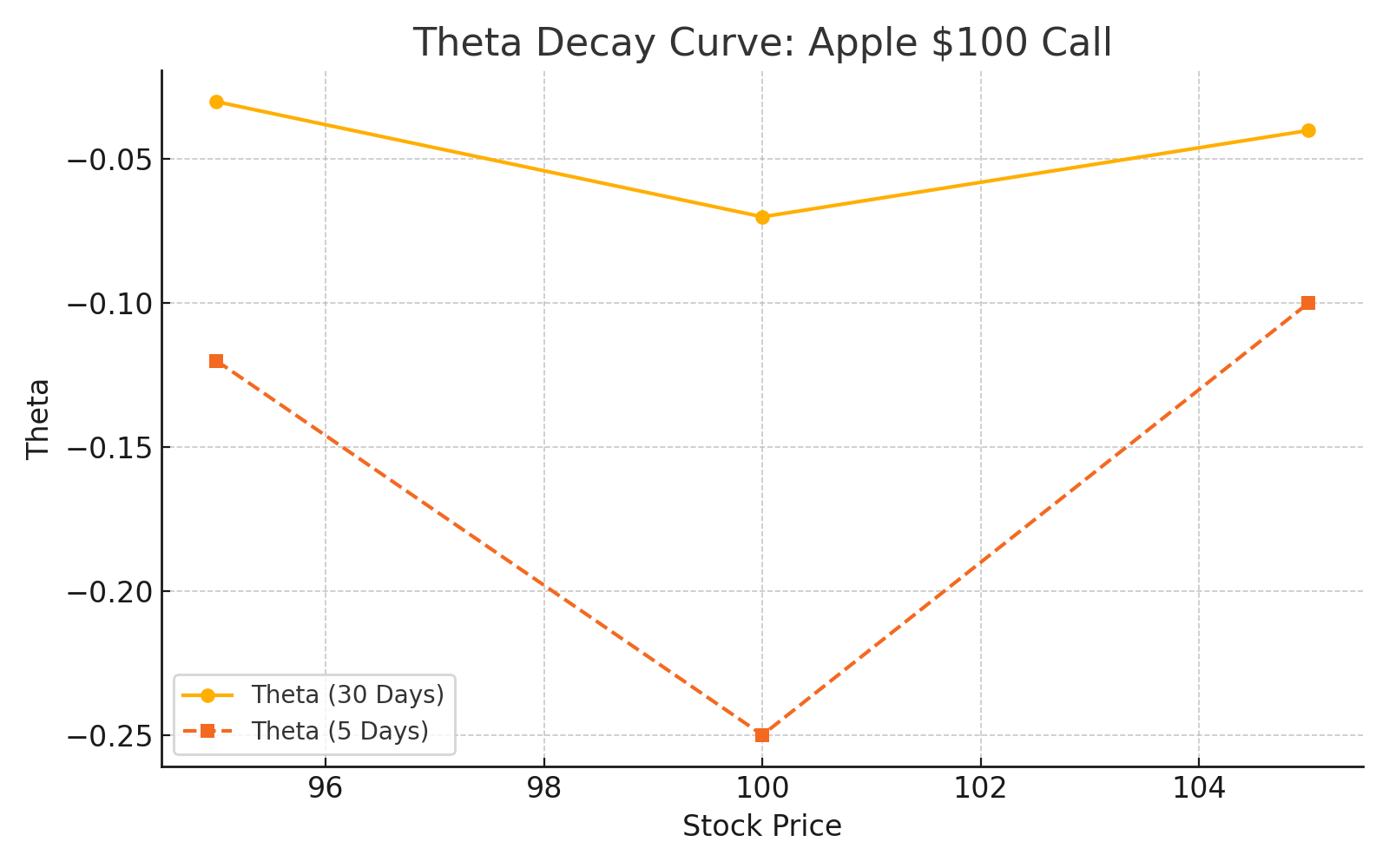

Theta in Action: 30 Days vs. 5 Days to Expiration

Here is a $100 call on Apple (AAPL) compared across two expirations, 30 days versus 5 days, to show how time decay accelerates as expiration approaches.

Chart: The Theta Decay Curve

How Traders Use Theta

⚡ Buy a short-dated option and the stock goes nowhere, and you still lose money every day, most sharply in the final week.

⚡ Sell options (credit spreads, cash-secured puts, covered calls) and that same decay is your income.

⚡ At-the-money options decay fastest near expiration; longer-dated options bleed slowly at first, then accelerate.

Vega (V)

V Definition

Vega measures the change in expectations for future volatility. It tells us how much an option's price will increase or decrease given a change in implied volatility.

Characteristics

- Higher volatility makes options more expensive since there's a greater likelihood of hitting the strike price

- Option sellers benefit from a fall in implied volatility, while option buyers benefit from a rise

- Long options have a positive vega and short options have a negative vega

- Vega can increase or decrease without price changes of the underlying asset due to changes in implied volatility

- Vega falls as the option gets closer to expiration

Practical Example

Vega is typically expressed as the dollar amount of change in the option price for a 1% change in implied volatility.

Trading Implications

When option prices are bid up because there are more buyers, implied volatility will increase. Long option traders benefit from pricing being bid up, and short option traders benefit from prices being bid down.

Traders can employ a vega-neutral position to offset the underlying asset's implied volatility. Options with longer expiration dates are generally more sensitive to volatility changes.

Vega in Action: Comparing 30-Day vs. 5-Day Options

Take at-the-money calls on Apple at two different expirations. Notice how Vega shrinks as expiration approaches:

Chart: Vega vs. Time to Expiration

How Traders Use Vega

⚡ Buy an at-the-money call right before earnings, watch the stock stay flat, and the option still loses value. That is implied volatility collapsing after the event.

⚡ Flip it: sell premium into that same event, the stock does not move, IV collapses, and Vega pays you alongside Theta.

⚡ LEAPs carry far more Vega than weeklies. Buying time means buying volatility exposure, so check where IV sits before you enter.

Rho (ρ)

ρ Definition

Rho measures an option's sensitivity to changes in the risk-free rate of interest (the interest rate paid on US Treasury bills) and is expressed as the amount of money an option will lose or gain with a 1% change in interest rates.

Characteristics

- Rho is positive for long calls (right to buy) and increases with the price of the stock

- Rho is negative for long puts (right to sell) and approaches zero as the stock price increases

- Rho is positive for short puts (obligation to buy), and negative for short calls (obligation to sell)

- Interest rate changes impact longer-term options much more than near-term options

- The higher the price of the stock and the longer time until expiration generally means a greater sensitivity to changes in interest rates

Practical Example: Positive Rho (Call Option)

⚡ Assume XYZ has a current market price of $50.00

⚡ Buying Stock Value: Buy 100 Shares XYZ at $50.00 per Share = $5,000.00 Total Cost

⚡ Buying Call Option: Buy 1 $50.00 Call at $10.00 Premium = $1,000.00 Total Cost

The total exercisable value of this option is $5,000.00 (right to buy 100 shares at $50.00). The cost to purchase the option ($1,000.00) is less upfront capital than the total exercisable value, the remaining $4,000.00 could be deposited and earn interest. This would be positively reflected in the value of the long call option as interest rates increase.

Practical Example: Negative Rho (Put Option)

⚡ XYZ has a current market price of $50.00

⚡ Shorting Stock Value: Sell 100 XYZ at $50.00 per Share = $5,000.00 Total Proceeds

⚡ Buying Put Option: Buy 1 $50.00 Put at $10.00 Premium = $1,000.00 Total Cost

The total exercisable value of this option is $5,000.00 (right to sell 100 shares at $50.00). The $5000.00 from a short sale could be deposited and earn interest. This would be negatively reflected in the value of the long put option as interest rates increase.

Trading Implications

Interest rate risk has the greatest effect on longer-dated options (LEAPS). Under normal circumstances, interest rates move gradually (~0.25% per quarter). Rho is generally less significant than other Greeks during stable interest rate environments but becomes more important in environments with significant interest rate changes.

Frequently Asked Questions About the Option Greeks

What are the option Greeks in simple terms?

They are five measurements of how an option's price reacts to different forces: Delta (stock price moves), Gamma (how fast Delta changes), Theta (time passing), Vega (volatility changes), and Rho (interest rates).

Which Greek is most important for beginners?

Delta. It tells you both how much your option will move per $1 change in the stock and, roughly, the probability the option finishes profitable. A 0.30 delta call has about a 30% chance of being in the money at expiration.

Is Theta good or bad for me?

It depends which side of the trade you are on. Theta is the buyer's enemy because the option loses value every day, and the seller's friend because that daily decay becomes the seller's profit.

What is a good Delta for selling options?

Many income traders sell options around 0.20 to 0.30 delta, which implies roughly a 70% to 80% chance the option expires worthless and the seller keeps the premium.

Is Delta the probability of profit?

Roughly, yes. Traders read a 0.30 delta as about a 30% chance the option expires in the money, which makes Delta a quick gauge of how aggressive or conservative a trade is.

What does Gamma mean in options?

Gamma measures how fast Delta changes when the stock moves $1. A 0.50 delta option with 0.05 gamma becomes a 0.55 delta option after a $1 rally.

Why is Gamma highest at the money?

Because that is where each $1 move has the biggest effect on the odds of finishing in or out of the money. Deep in- or out-of-the-money options barely change their behavior, so their Gamma approaches zero.

Is high Gamma risky?

For sellers, yes: high Gamma means the position's exposure can swing quickly, which is why short options get riskier near expiration when Gamma peaks. Buyers experience it as acceleration in their favor when the move goes their way.

What does Theta mean in options?

Theta is the amount of value an option loses each day from time passing alone. A theta of -0.05 means the option sheds about $5 per contract per day, all else equal.

Why does Theta accelerate near expiration?

Time value reflects the chance of a meaningful move before expiry. As days run out, that chance collapses faster and faster, so the final weeks see the steepest decay.

What does Vega mean in options?

Vega measures how much an option's price changes for each one-point move in implied volatility. A Vega of 0.10 means the option gains or loses about $10 per contract when IV rises or falls one point.

Why does my option lose value after earnings even when I was right?

IV crush. Implied volatility inflates before the event and collapses after it, and Vega translates that collapse into a price drop that can overwhelm the directional gain.

Which options have the most Vega exposure?

Longer-dated and at-the-money options. If you are buying time, you are also buying volatility exposure, so check where IV sits relative to its normal range before entering.

Keep Learning

📘 Options Break-Even Prices Explained

📘 Implied Volatility Explained

📘 Options Time Decay Explained

The Greeks finally click when you use them on real trades. That's how we teach them in the Options Trading in 21 Days course.

Stay Connected!

Join our mailing list to get notified of all new blog posts, and receive the latest news and updates from our team.